When it comes to investing in foreign assets, currency direction can dramatically improve or reduce your investing performance. In the short run (month to month), it’s a gamble. And for over 25 years in wealth management, I’ve avoided taking a directional view on the U.S. dollar….until now.

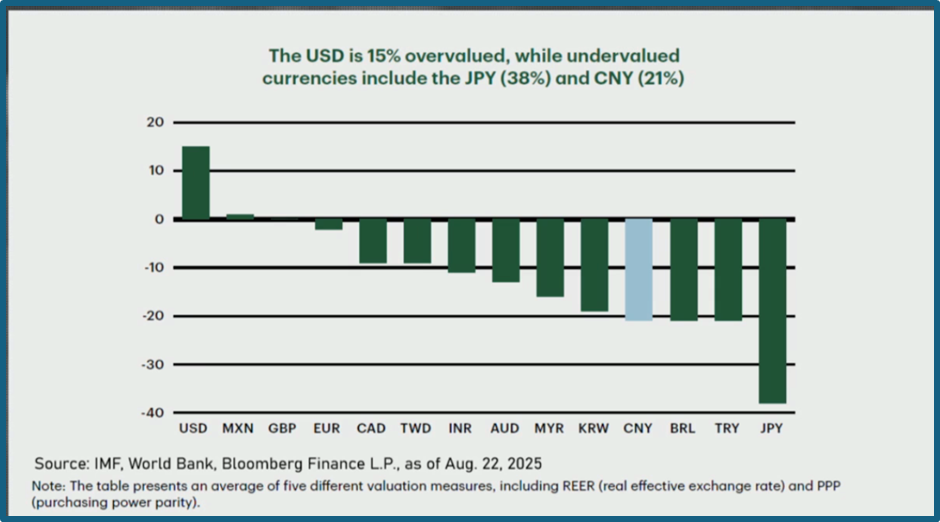

As the PM of the Oasis Growth Fund based in Canada, the outlook for the US economy is still very favourable, so I intend to remain invested. Yet, I am in full agreement with Kevin Hebner, Managing Director and Global Investment Strategist at TD Epoch, that the USD is 15+% overvalued (Chart #1), and that a weaker USD is inevitable over the next few years.

Chart 1: The USD is 15% overvalued. Source: IMF, World Bank, Bloomberg L.P. as at Oct 22, 2025

1. Structural Fiscal Pressures

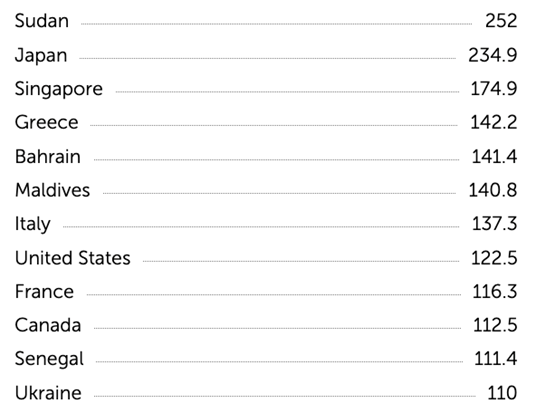

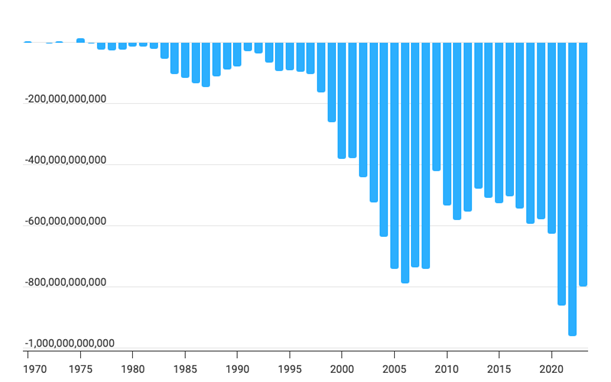

- U.S. debt-to-GDP is now over 120% — 5th highest globally (Chart #2)

- Debt servicing cost ($900B annually) is the 4th largest U.S. budget item.

- Persistent deficits require issuing more Treasuries. Increased supply pressures the $USD.

IMF 2025 Government Debt to GDP Top 12 Countries

Chart 2: IMF 2025 Government Debt to GDP Top 12 Countries. Source: IMF as at Oct 15, 2025

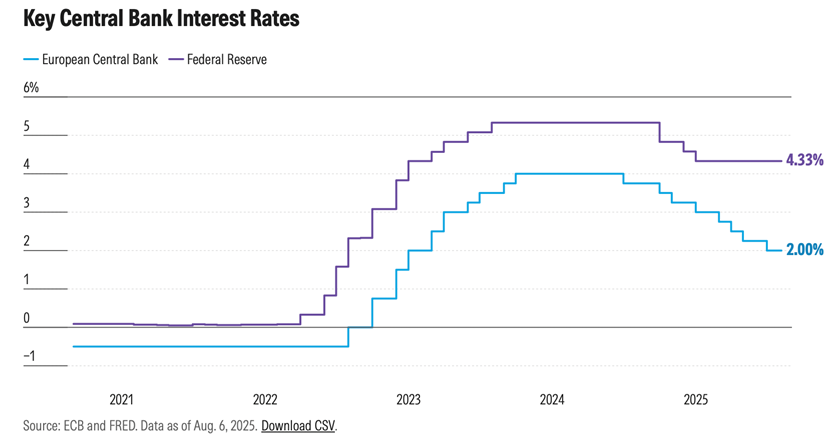

2. Interest Rate Coverage

- The Fed is expected to cut rates as inflation cools. With U.S. yields falling closer to peers, the dollar’s rate advantage will fade.

Chart 3: Key Central Bank Interest Rates. Source: ECB and FRED August 6, 2025

3. Reverse Diversification

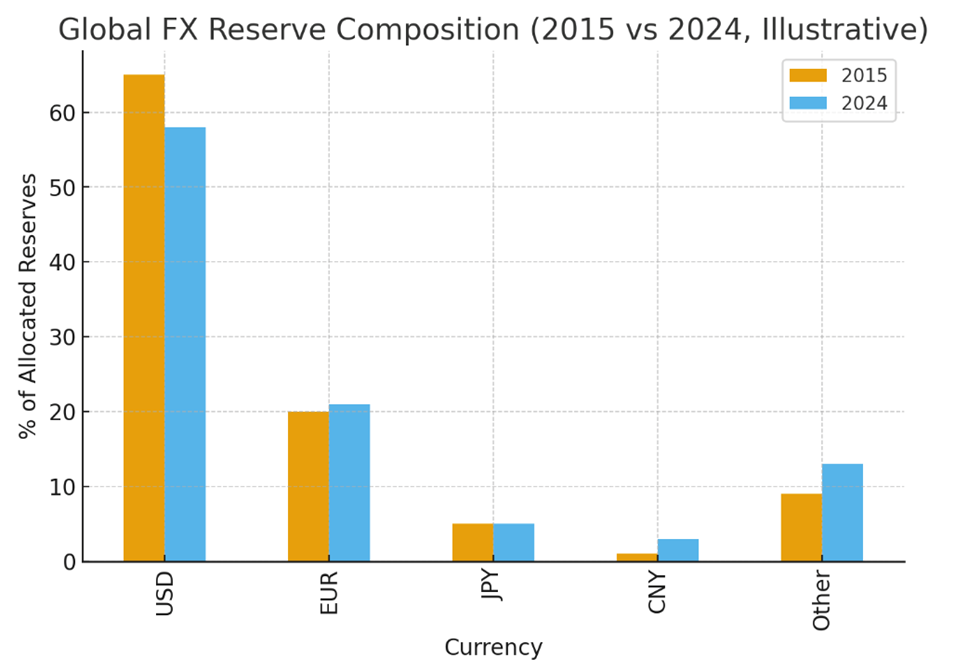

- Central banks globally are reducing reliance on the $USD, shifting to gold, euros, and yuan. Sanctions policies have accelerated this trend

Chart 4: Global FX reserve Composition. Source: Bloomberg Financial

4. US Trade & Current Account Deficits

- The U.S. imports far more than it exports. An imbalance requires constant foreign capital inflows. When capital inflows slow, the dollar weakens. A need for capital may require a premium on long-term US Treasuries.

Chart 5: Persistent U.S. Trade Imbalance. Source: Macrotrends

5. Shifts in Capital Flows

- Foreign investors have forever demonstrated an insatiable demand for US assets (Chart #6) But it has reached epic proportions. Today 85% of the US GDP is now attributable to foreign investments, up from 12% twenty years ago

- Global money is now moving into emerging markets — and political risks in Washington could accelerate that shift.

Chart 6: Foreign ownership of U.S. equities. Source: U.S. Treasury, Federal Reserve Board August 22, 2025

6. Policy Direction

- The US administration is attempting to manipulate the US trade imbalance by imposing trade tariffs and purposefully actioning policies in support of a weaker $USD.

- The administration is also seeking to usurp control over US the Federal Reserve board. The loss of Fed independence in the Spring of 2026 would further undermine the $USD.

The Bottom Line

The $USD still has deep liquidity, safe-haven status and remains the global reserve currency, but the headwinds are undeniable. Can the positive impact of AI technology, domestication of the Chip Industry, and American reindustrialization be enough to counteract a decline in the $USD?

For Investors

- Stay invested. U.S. companies remain innovative and profitable.

- Buy quality. Stand your ground. The economic outlook is still favorable.

- Hedge your $USD exposure. Be patient. This is a secular strategy.

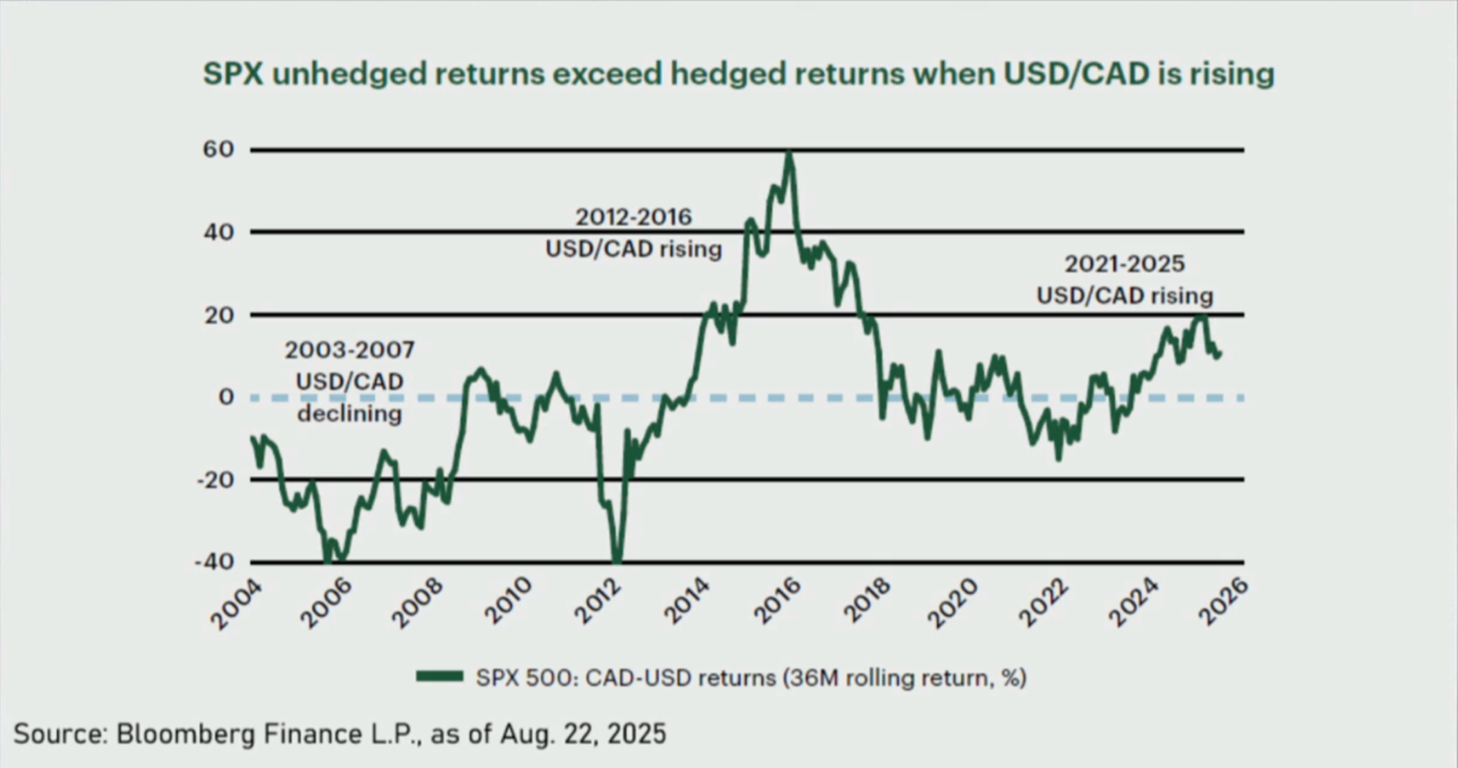

As per chart #7, during the last decade, a strengthening $USD boosted returns for Canadian investors. Over the next few years, $USD exposure is likely to be detrimental. If uncertain how and when to deploy a hedge, consider investing with a fund manager willing to implement just such a strategy. The Oasis Growth Fund deploys such tactical hedges.

Chart 7: SPX unhedged returns exceed hedged returns when USD/CAD is rising. Source: Bloomberg Finance L.P. August 22, 2025

Disclosures

This investment memorandum expresses the views of the author as of the date indicated and such views are subject to change without notice. Fieldhouse Capital Management Inc. (herein “Fieldhouse”) has no duty or obligation to update the information contained herein. Further, Fieldhouse makes no representation, and it should not be assumed, that past investment performance is an indication of future results.

The return of the Oasis Growth Fund is based on monthly total returns of the Fieldhouse Pro Funds Trust – Series O Oasis Growth Fund in Canadian dollars since inception at January 1st, 2020. All returns are time-weighted total returns of the F class, net of fees, and annualized for periods one year or greater.

Fieldhouse Capital Management Inc. is the Investment Fund Manager, Portfolio Manager and trustee of Fieldhouse Pro Funds Trust Advisor Series funds. Fieldhouse Pro Funds Trust funds are subject to management fees, trailing commissions, incentive fees and administration fees. For detailed information on fees see the the Fieldhouse Pro Funds Trust offering memorandum and the Series O offering memorandum supplement or the term sheets.

The Series O Oasis Growth Fund of Fieldhouse Pro Funds Trust was previously Class O of Fieldhouse Pro Funds Inc. The fund changed it’s investment strategy and it’s name from the “Oasis Canadian Growth++ Income Fund” to “Oasis Growth Fund” on January 1st, 2020. The fund NAV was reset to $10 at that time. The funds strategy changed from a Canadian growth and balanced fund to the North American Growth fund described on this page and in the Fieldhouse Pro Funds Trust offering memorandum. Class O of Fieldhouse Pro Funds Trust was previously Class B of Fieldhouse Pro Funds Inc. which had an inception date of April 1 2016. Fieldhouse Pro Funds Inc. converted to Fieldhouse Pro Funds Trust on January 1st, 2022. Historical fund performance for previous strategies is available on request. The Fieldhouse Pro Funds Trust offering memorandum and the Series O offering memorandum supplement contain additional information that should be considered by all investors prior to investing.

This memorandum is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. There are many important factors to consider when investing and you should seek professional advice that can assess your personal circumstances and risk appetite. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Fieldhouse believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This memorandum, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of Fieldhouse.